How to Fight Bank Fees Effortlessly

Bank fees are charges that a bank or financial institution imposes on its customers for various services. These fees can be for everything from using an ATM to maintaining a checking account. While some fees are mandatory, such as monthly service charges, others may be avoidable.

An excessive amount of can easily cut into your base checking and savings funds. That's why it's essential that you have a thorough understanding of how these fees work and how to avoid being charged unnecessarily.

In this article, we will describe common bank fees and how you can not only avoid them but dispute any that may have been applied to your account in error. In addition, you will discover how DoNotPay is the fastest and easiest way to .

About Bank Fees

A is a business like any other. They charge fees to make a profit and pay operating expenses. More specifically, financial institutions charge fees for the following reasons:

1. Fees help banks stay profitable and increase their bottom line.

2. Fees help banks stay afloat during tough times.

3. Cover the cost of providing banking services.

4. Banks offer a variety of services that come with different costs.

What Are the Most Common Bank Fees?

The most common fees charged by banks are as follows:

| Account maintenance and minimum balance: | These generally range from $5 to $25 per month. The more rewards and other benefits they have, the higher this fee may be. |

| ATM fees: | Banks charge an ATM fee for using machines that are not affiliated with the bank. There is an ATM provider fee and a bank fee. Both can typically be $4 per transaction. |

| Overdraft: | Even though you may have a backup account in the event you don't have enough funds to cover a payment, the bank will typically charge you $10 to $12 for each overdraft. |

| Insufficient funds: | If you do not have a backup account to cover the funds, most banks charge a $35 insufficient funds fee. |

| Excess transactions: | Many banks limit the number of withdrawals you can make in a month. Once you surpass the number of allowed withdrawals, banks charge anywhere from $3 to $25 per transaction. |

| Wire transfer fees: | Wire transfers can be a quick way to send money, but it comes at a cost. Banks typically charge from $16 to $35 per wire transfer. |

How You Can Minimize Bank Fees

Even though banks charge various , there are ways to avoid some of them. Here are some proven tips:

| Sign up for free, or low-cost checking and savings accounts: | Many banks offer free accounts for keeping a minimum balance. |

| Use direct deposit: | By having your paycheck deposited automatically, many banks will waive maintenance fees. It will also protect you against overdrafts since the funds are available immediately after deposit. |

| Keep a minimum balance: | By keeping the minimum balance required in the account, you can avoid monthly fees. |

| Have multiple accounts at the same bank: | For example, having both a checking and savings account at the same bank, can save you overdraft and insufficient funds fees since the balance is taken from the other account. Banks may also waive fees for being a long-time customer in good standing with multiple accounts. |

| Use only your bank's ATM: | Take out larger withdrawals to avoid having to use out-of-network and incur fees. |

| Sign up for email or text alerts: | Many banks have automatic email and text alerts to notify you when your balance falls below a certain level. |

The Best Banks With Minimal Fees

Though most banks charge fees, there are a handful of online financial institutions that stand out for no or low fees. These are as follows:

- Axos Bank Axos is a full-service online bank. They have no monthly maintenance fees or minimum balance requirements. They also provide unlimited reimbursement for domestic out-of-network ATM charges. Not only that, but they also do not charge a non-sufficient funds fee. They offer many types of checking accounts with varying rewards. Savings accounts only require $250 to open, but there are no balance requirements.

- PenFed Credit Union Access America Checking PenFed charges a monthly maintenance fee of $10, but if you have at least $500 in direct deposits or maintain a daily balance of at least $500, this fee is waived. The regular savings account has no maintenance or other monthly fees. ATM withdrawals are just $1.50 and balance inquiries are $1.00 at in-network and non-PenFed ATMs.

- Discover Cashback Debit Checking Discover has a no-fee checking account that offers cashback rewards of 1%, up to $3,000 in debit card purchases each month. There are also no fees for account maintenance, in-network ATMs, or online bill pay. There are no minimum balance requirements. They also offer a no-fee savings account with no minimum balance requirements.

- NBKC Bank NBKC Bank's Everything Account combines checking and savings into a single account. There are no monthly maintenance fees or minimum balances. There are also no fees for overdrafts, returned items, money orders, or stop payments.

- TIAA Bank Yield Pledge Checking TIAA Bank only requires a $100 deposit in their Basic Checking account and a $25 minimum account balance to avoid a $5.00 monthly maintenance fee. ATM fees are waived if the account has a balance of $5,000 or more. For those under that amount, up to $15 in ATM fees are reimbursed monthly. There are no fees for a savings account with at least a $25 minimum balance.

How to Dispute Bank Fees by Yourself (it’s Not Easy)

Unless fees were applied in error or the customer was not told about them upfront, banks will not remove their fees. However, if you need to dispute a fee with your bank, here is a typical dispute process to follow:

- Contact the bank as soon as you realize you've been wrongly charged. Have documented proof of the error in your statements.

- Provide a timeline and explain why you believe the charge is in error.

- If applicable, point out the fact that you are a long-time customer. Sometimes banks will show their appreciation by negotiating their fees.

- If the representative you are working with isn't helpful, ask to speak to a supervisor or manager.

- As a last resort, you can say you may take your banking business elsewhere if they don't reduce or remove the fees in question.

DoNotPay Has an Easier Way to Fight Bank Fees

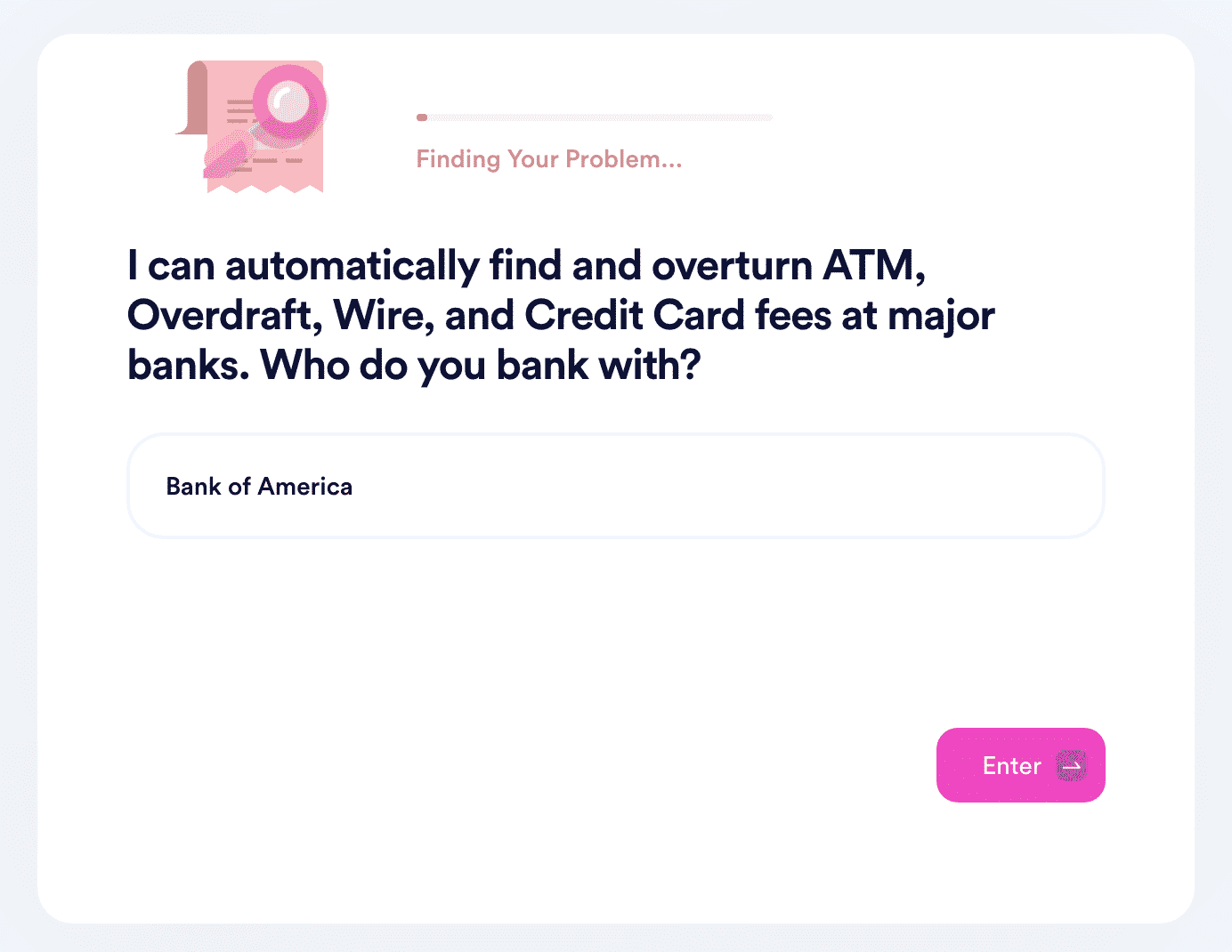

If you want to get your bank fees waived, but don't know where to start, DoNotPay has you covered in four easy steps:

- Open the DoNotPay Fight Bank Fees product.

- Enter the name of your bank.

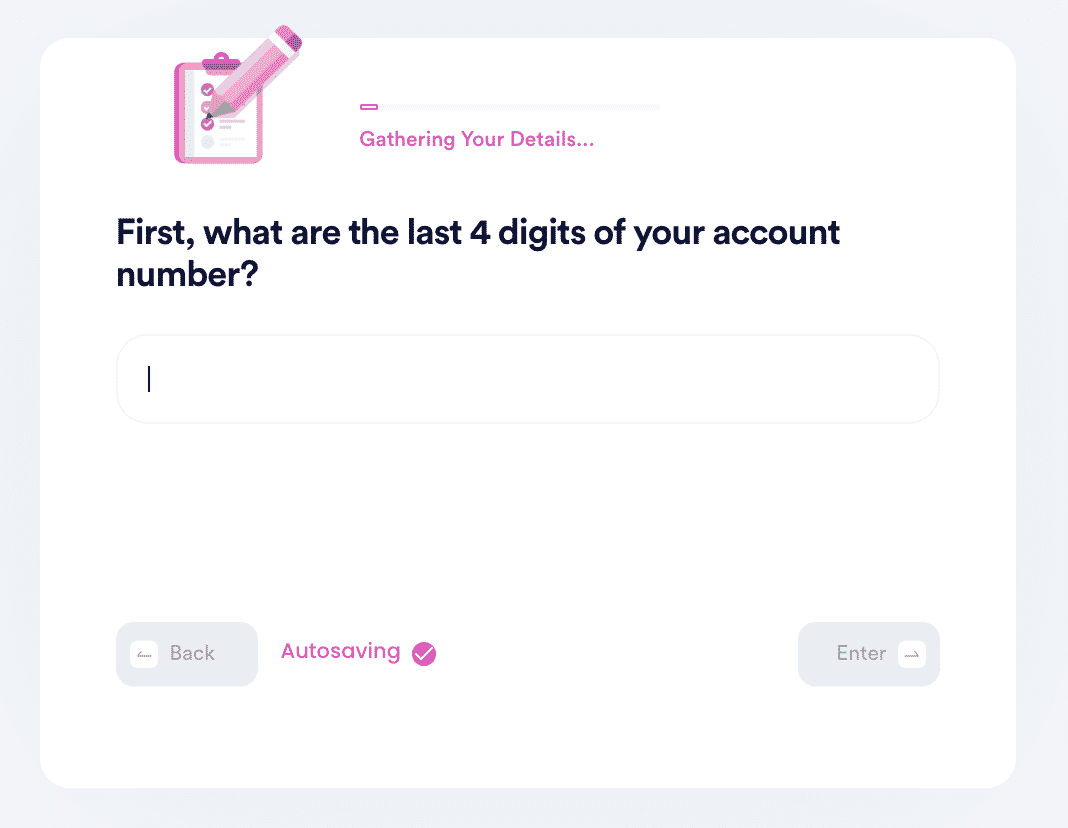

- Verify the last 4 digits of your bank account.

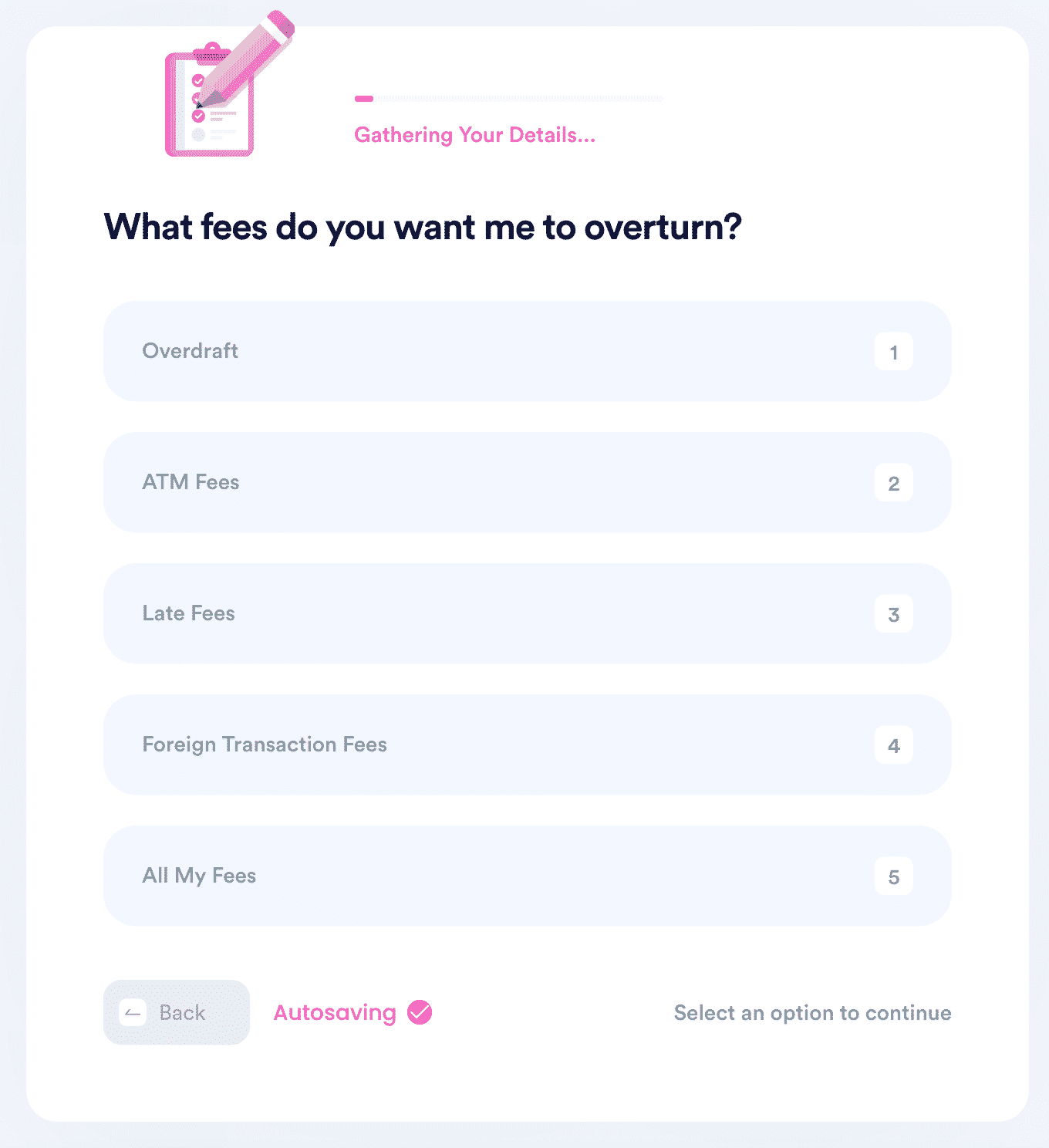

- Choose which fees you want to waive, including overdraft, ATM, and transaction fees.

DoNotPay Can Help You Dispute Other Bank Fees

In addition to assisting with disputing fees in general, DoNotPay can help with the following related financial issues:

- Citizens Bank overdraft fees refund

- Chase Bank overdraft fees refund

- PayPal transfer to bank fee

- Overdraft fees on weekends

- Bank of America ATM fees

- Fifth Third bank overdraft fees

- Bank of America overdraft fees refund

- TD Bank overdraft fees

- Finding banks without overdraft fees

- Wells Fargo Checking account overdraft fees refund

What Else Can DoNotPay Do?

DoNotPay works with all companies, groups, and entities to resolve common administrative issues such as the ones listed below:

- Appeal banned accounts

- Cancel any service or subscription

- Get gift card cashback

- Create a power of attorney

- Solve credit card problems

- Use a fake phone number

- Help with bills

- Chargebacks and refunds

- How to write a financial aid appeal letter

With the innovative web-based platform, DoNotPay cuts through red tape to resolve your problems faster and easier than if you were to do it yourself. Try it today.

AI that fights for you

AI that fights for you