All About the HSA Bank Fee Schedule and How to Fight Them

If you are lucky enough to have insurance through your employer, you may have noticed the option to enroll in a health plan with a health savings account (HSA). If you took advantage of this savings account, watching your balance grow tax-free could have you considering increasing your contributions.

On the other hand, account fees might have you wondering if an HSA is as good a deal as it's said to be. If you would like to , DoNotPay can help.

Who Can Have a Health Savings Account (HSA)

To be eligible for an HSA, you must be enrolled in a high-deductible health plan and not claimed as a dependent on someone else's tax return. Many people get their HSA through their employer, but you can open one on your own. If you do not have an employer-offered option, you will miss out on some of the tax benefits, so you may want to consider other investment options.

Benefits of an HSA

While it is a good savings strategy to keep your medical savings in a separate bucket from your other funds, your HSA can be so much more than that. Your HSA is a triple tax-advantaged account:

- Tax-Free Contributions: Like a traditional 401k, your HSA contributions are made pre-tax from your paycheck.

- Tax-Free Growth: Like a Roth IRA or 401k, you are not taxed on the growth of your HSA if you invest it.

- Tax-Free Qualified Distributions: If you withdraw funds for medical needs, you are not taxed on them. If you withdraw for non-qualified distributions, you will pay tax on the funds at your regular income tax bracket. If you are under 65, there is an additional 20% penalty.

Note that an HSA is different from a flexible spending account (FSA). The money rolls over from year to year. With all the benefits your HSA gives you, it matters where you keep your account. If you're constantly being charged by the bank, your money doesn't have a chance to grow.

Potential Fees at HSA Bank

HSA Bank account holders have three fees to keep in mind:

- Monthly Maintenance Fee - HSA charges $ 2.50. You can have this fee waived by maintaining a minimum balance of $3,000 every statement cycle.

- Paper Statement Fee - Members are automatically enrolled in digital statements. You can opt out for a monthly charge of $ 1.50.

- Account Closing Fee - If you have an account through your employer and you switch jobs, you may wish to transfer your funds to your new account to avoid inactivity fees eating away at your balance long-term. Account closure fees are $ 25.

There is an investment balance minimum, so you do have to leave your funds in the savings portion of the account. Fortunately, those funds can still work for you by earning interest. There are three interest earning tiers:

- Less than $5,000

- Between $5,000 and $25,000

- More than $25,000

As with other savings accounts, interest rates vary.

Investment Fees

HSA Bank offers two options for self-managed investing within your account:

- Devenir HSA - With this option, you are limited to investing in mutual funds. You may see an annual service fee of 0.3% on your account. , so the actual amount on your statement would be 0.075%. The minimum fee you would be charged is $1.50, so if you have less than that amount in your account when you are charged, all your holdings will be sold to pay the fee.

- TD Ameritrade HSA - TD Ameritrade HSA investors have access to everything they would in a traditional brokerage account. There is no fee for trading US stocks or ETFs. There is also no fee for many types of mutual funds, though trading the same no-load mutual funds available through the Devenir would get you charged $25 per transaction. If you do choose to invest in ETFs, you must also be mindful of the expense ratio if you want to keep fees low.

If you do choose to invest part of your HSA, there is an additional fee to watch out for. If you do not have at least $5,000 in your HSA not including the invested portion, you will be charged $3 a month.

Protecting Your Funds at HSA Bank

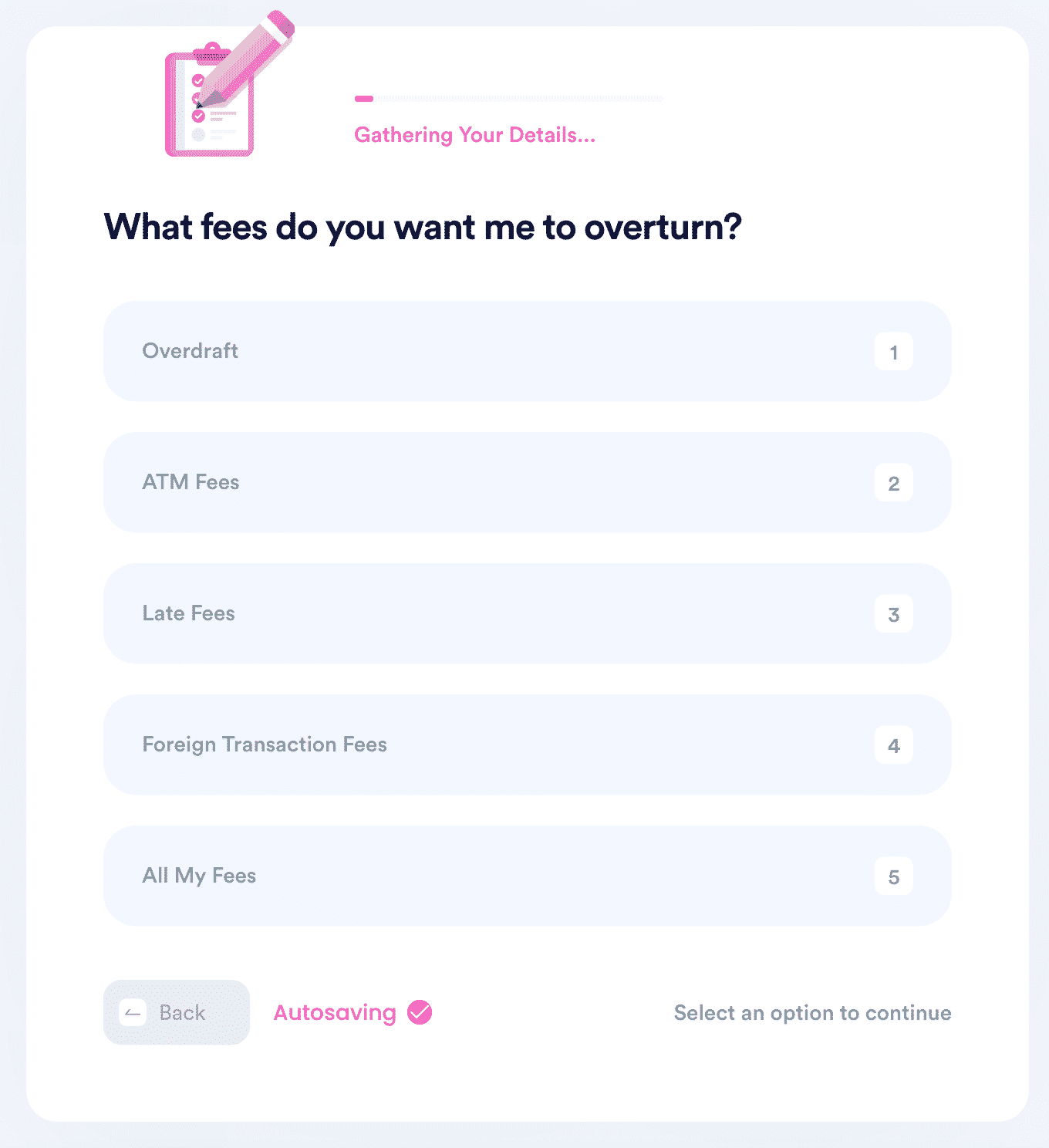

If you want to but don't know where to start, DoNotPay has you covered in 4 easy steps:

- Open the DoNotPay Fight Bank Fees product.

- Enter the name of your bank.

- Verify the last 4 digits of your bank account.

- Choose which fees you want to waive, including overdraft, ATM, and transaction fees.

Keep Surprise Charges Off Your Statements with DoNotPay

You work hard for your money, and you should get to choose how it is spent. If you find your money just seems to disappear paycheck after paycheck, let DoNotPay help you keep more of it.

Here are other accounts DoNotPay can help you with:

| Bank of America overdraft fees | Chase Bank | Fifth Third Bank overdraft fees | Citizens Bank overdraft fees |

| Bank of America | Paypal | Wells Fargo | TD Bank |

What Else Can DoNotPay Do?

DoNotPay can assist you with:

- Find banks without overdraft fees

- Reducing your Property Taxes

- Applying for scholarships

- Canceling unused subscriptions

- Getting cash for unwanted gift cards

- Lowering your bills

and more. Try DoNotPay today to take more control of your finances!

AI that fights for you

AI that fights for you