Do Banks Charge Overdraft Fees on Weekends?

Of late, given the coronavirus pandemic, a number of banks have been criticized for charging overdraft fees, given that these target people who are already financially stretched. This doesn't mean that banks have stopped charging overdraft fees altogether, but many banks have reconsidered their position with regard to these fees. As of now, whenever you don't have sufficient funds in your account to cover your purchases.

However, you don't have to accept overdraft fees as a matter of course. There are ways to get around these fees, such as opting for a bank that doesn't charge them. You can also get overdraft protection which results in having to pay a lower fee. Or you can simply call up your bank and ask them to waive an overdraft fee that they may have charged.

These methods of battling overdraft fees may, however, be time-consuming. Plus, you might end up paying a smaller amount anyway. It might be a better idea to use DoNotPay to get all your bank fees waived, including the overdraft fees charged on weekends. The process is extremely simple; it only involves telling DoNotPay the last four digits of your bank account number and the name of your bank. After that, it's up to DoNotPay to simplify your life.

What Is an Overdraft Fee?

If you've never been charged an overdraft fee, it may take you by surprise. There are a few different types of fees associated with overdrafts.

| Overdraft Fee | Basically, an overdraft fee is charged when you don't have enough funds in your account to cover your purchases. For example, if you go to a store and spend $25, but you only have $15 in your account, the bank might go ahead and let you make your purchase, but it will also slap a $35 fee on your account, thus leaving your balance at negative $45! |

| Non-Sufficient Funds Fee | This is also referred to as the NSF fee. Once again, this fee is charged when you don't have sufficient funds in your account to cover your purchases. The difference between this fee and the overdraft fee is that the bank doesn't cover your purchases in this one but slaps you with a fee all the same. So, for example, when you try to make a purchase of $25 but you only have $15 in your account, then your charge is declined, and you're charged a non-sufficient funds fee. |

| Overdraft Protection | Obviously, the overdraft fee and the non-sufficient funds’ fee are very high and difficult for customers to pay. So banks came up with overdraft protection, in which you can link a savings account or a credit card to your checking account. And if you try to make a purchase that goes over your balance, the bank deducts that money from your savings or checking account and charges you a lower fee which is around $10-$15. |

| Extended Overdraft Fee | As if it weren't enough that you had to pay a hefty overdraft fee for just overspending by $10 or so, there's another fee that banks charge when you don't rectify the situation in a few days. If you don't bring your account balance back up over zero, many banks will charge you an extended overdraft fee every 5-7 days, in addition to the original overdraft fee. |

Why Are Overdraft Fees Charged?

At times, the overdraft fee is just a result of the customer not realizing that there are insufficient funds in his/her account. But, at other times, it may occur because the bank has not yet finished processing a deposit.

For example, maybe you just deposited a check from the place where you work, so you think that you have ample funds in your account. But it actually takes banks a few days to process checks. So if you make any purchases before the check has gone through, you may be charged an overdraft fee.

Many banks have been re-thinking this strategy, however, and some of them have started giving customers a 24-hour grace period to rectify the overdraft situation.

Are Overdraft Fees Charged on the Weekend?

The short answer to this question is: yes, . It doesn't matter when you make the purchase for which you don't have sufficient funds in your account. If the bank is one that usually charges overdraft fees, it will charge you overdraft fees on the weekend as well.

But once again, if you are banking with a bank that gives you a 24-hour grace period, then you'll have that time to deposit funds into your account. Plus, many banks have now placed a limit on the number of overdraft fees they will charge in a day (in case you do more than one transaction that goes over your bank balance).

Switching to a Bank That Does Not Charge Overdraft Fees

There are many ways in which you can avoid overdraft fees. You might want to open an account with a bank that doesn't charge overdraft fees such as:

- Axos Bank

- Discover Bank

- NBKC Bank

- Chime Bank ($20 overdraft allowed on debit card purchases)

- Huntington Bank (24-hour grace period and $50 safety zone)

What Else Can You Do to Avoid Paying Overdraft Fees?

If switching banks is not practical for you at this point in time, take one of the following steps:

- You can download your bank's mobile banking app and keep checking your balance to make sure that you don't go over it.

- Keep in mind that direct deposits, cash deposits, and wire transfers become available immediately, but checks might take 1-7 days to go through. So don't spend the money until you are sure it's available for use.

- Many banks give you the option of getting overdraft protection, but this is not immediate. You have to speak to someone at the bank to have it activated. Doing this will mean that the funds will be taken from your savings account/credit card and you will pay a lower fee.

- If you have been charged an overdraft fee, you can always call the bank and ask them to waive it as a courtesy, especially if you haven't overdrawn your account before. This is not guaranteed to work, but it does, in some cases.

How to Avoid Overdraft Fees Using DoNotPay

When you're already financially challenged, it can be difficult to have to pay an overdraft fee or a non-sufficient funds fee. And if the overdraft occurs over the weekend, you may feel like there's nothing you can do about it.

However, there are many ways to combat overdraft fees and any other fees that banks and financial institutions may charge you. You don't have to submit to these fees just because they've always been charged.

Still, changing banks or keeping track of your account balances at all times may not be practical. In such cases, you can turn to DoNotPay for help in getting your overdraft fees waived. By just answering a few simple questions, you can give DoNotPay all the information needed to get your overdraft fees waived.

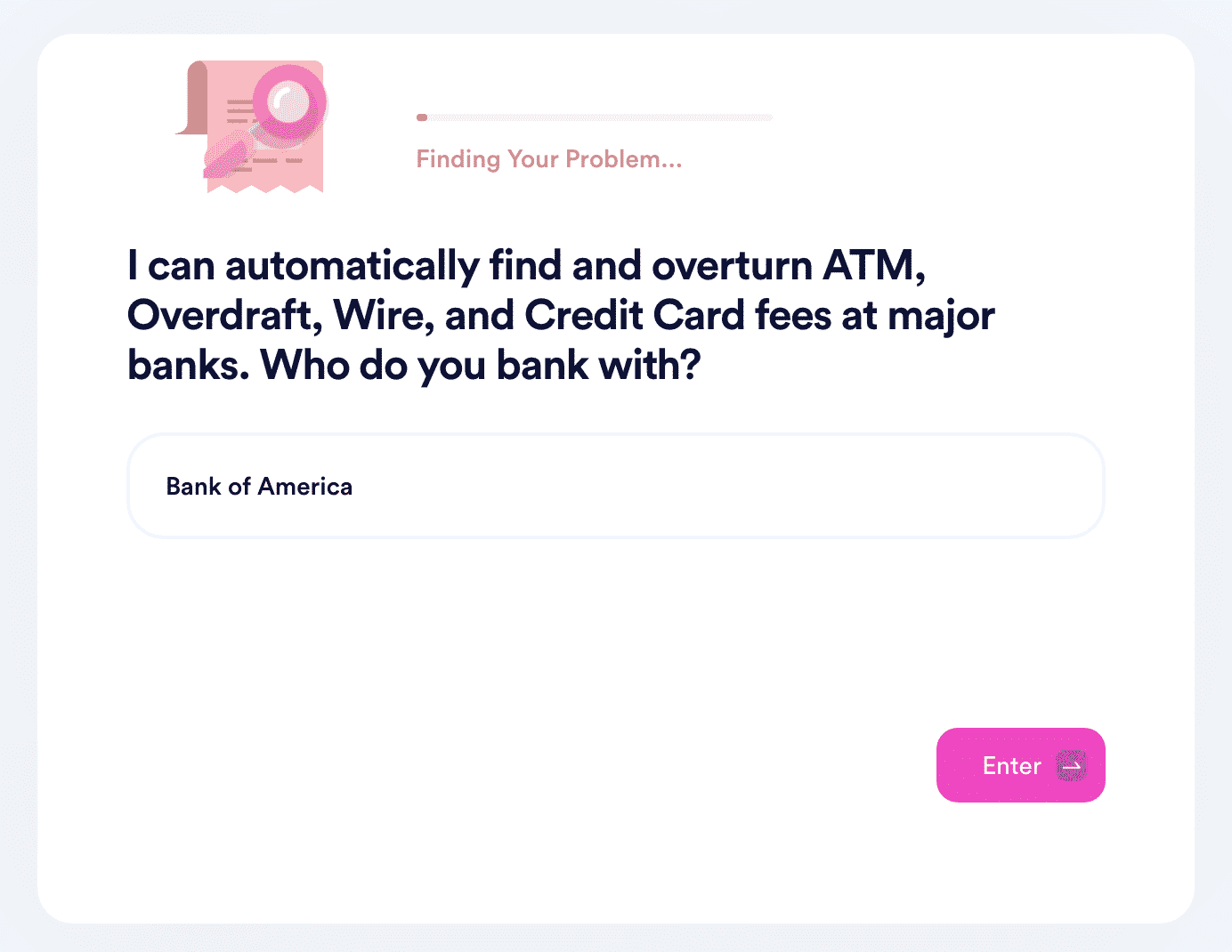

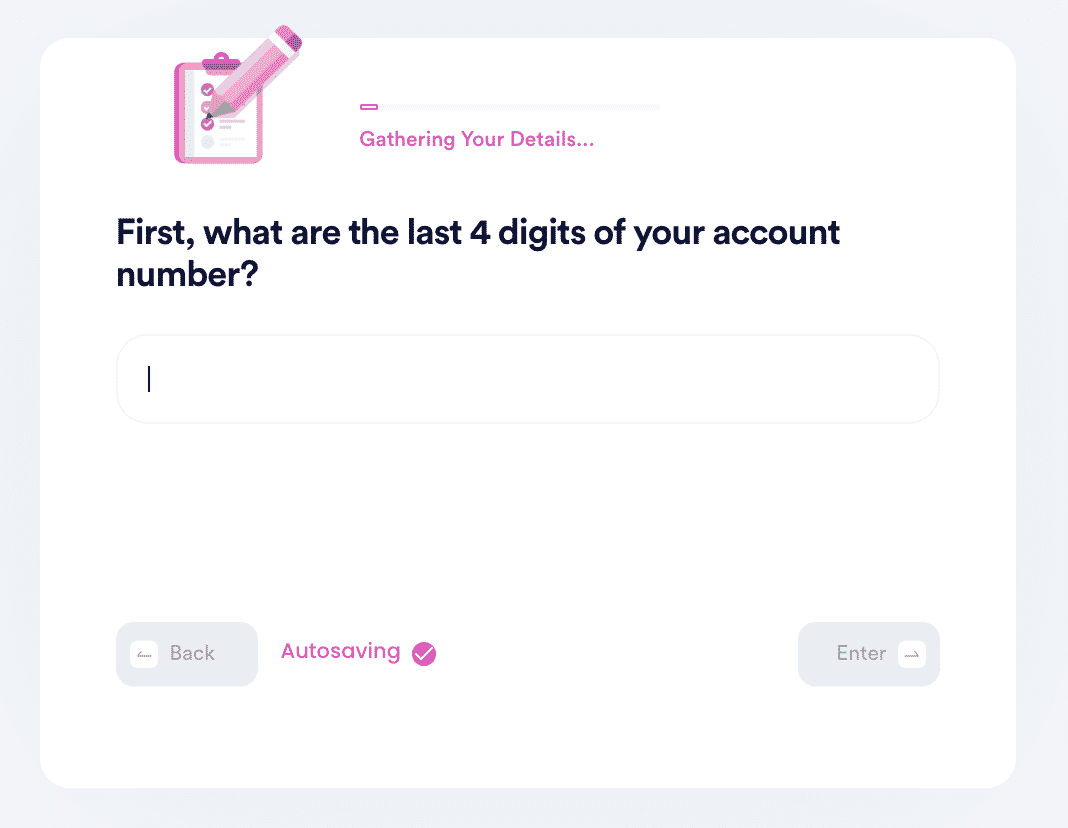

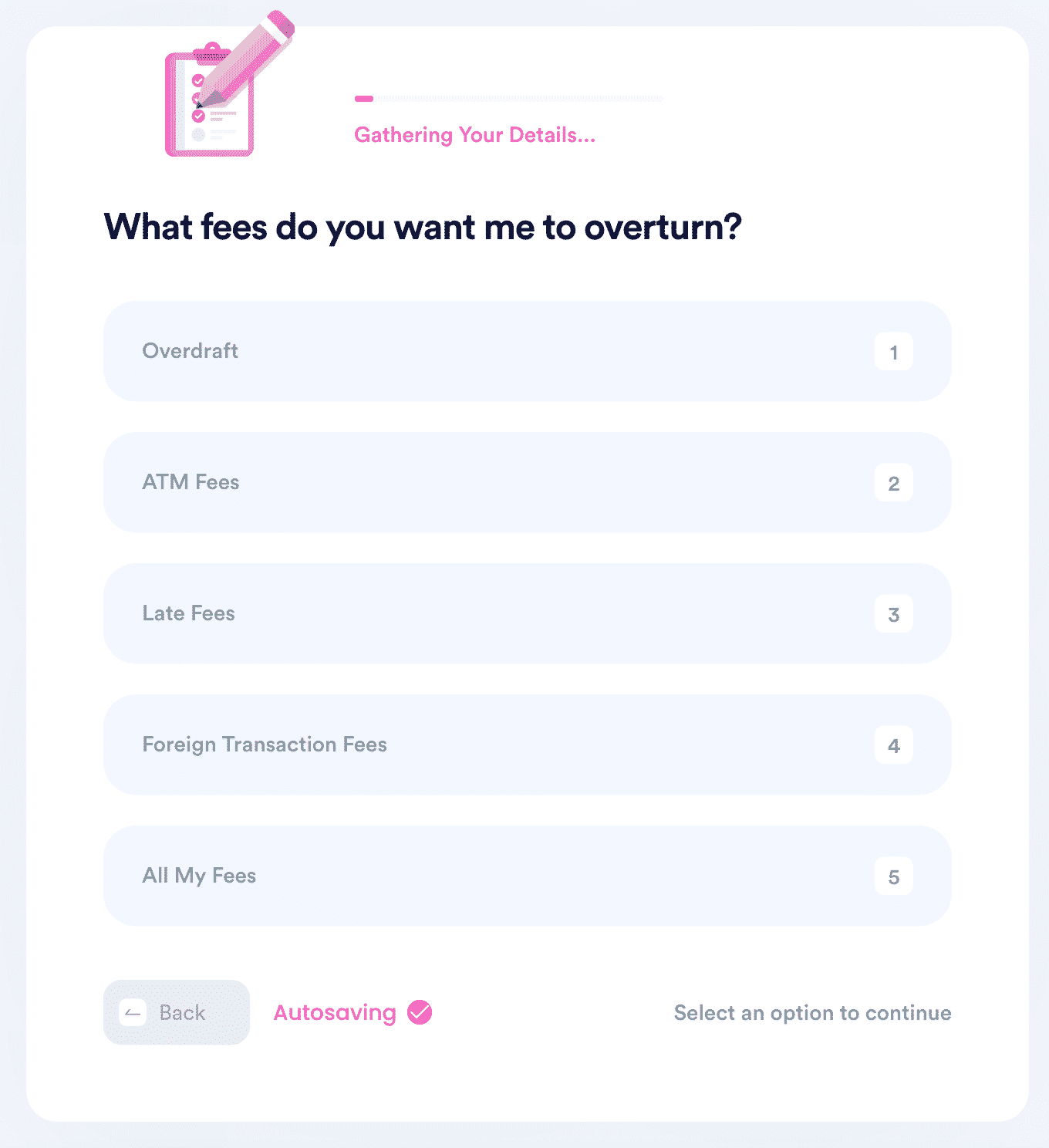

If you want to get overdraft fees waived with DoNotPay but don't know where to start, DoNotPay has you covered in 4 easy steps:

- Open the DoNotPay Fight Bank Fees product.

- Enter the name of your bank.

- Verify the last 4 digits of your bank account.

- Choose which fees you want to waive, including overdraft, ATM, and transaction fees.

Overdraft fees, non-sufficient funds fees, overdraft protection fees, and extended overdraft fees can be difficult for an average person to pay. When you're already financially overstretched, these fees stretch you even further, leading to a complete deterioration in your financial condition.

What Else Can DoNotPay Do?

Fortunately, DoNotPay can help you to combat fees and any other fees that your bank may demand from you. That include:

- Bank of America overdraft fees

- Chase Bank overdraft fees

- TD Bank overdraft fees

- Bank of America ATM fees

- Paypal transfer to bank fee

- Fifth Third Bank overdraft fees

- Citizens Bank overdraft fees

- Wells Fargo checking account overdraft fees

- And many more!

By going to DoNotPay, you can take the first step towards financial solvency.

AI that fights for you

AI that fights for you