Request a Credit Limit Increase From WECU Fast

Remember how thrilled you were when you got your first credit card? And, did you think you'd ever reach your credit limit? Well. Times change, life gets more expensive, and these days, that credit limit seems rather paltry when you compare it to your actual needs. DoNotPay is here to help you learn how to ask for an—keep reading to find out how to get the credit you deserve.

Credit or Debit?

We've all heard that a million times, but what exactly does it mean? Did the credit union give me a Visa and not tell me? No, they didn't.

First, let's discuss how credit cards work. Since Visa also issues debit cards that are considered "debit" or "credit" at the same time, it can be a little confusing when you get your first WECU Visa card or your first debit card.

- A credit card is completely independent of your checking or savings account at WECU

- A debit card pulls money from your checking account every time you make a purchase

The credit or debit question is more of an operational issue for the vendor. If you use your PIN, the transaction runs as a debit. If you skip the PIN, the vendor pays the credit card transaction fee. Either way, the money leaves your account right away, so please don't think that if you use the "credit" feature, there's some magic Visa that's paying for your stuff.

How Do Credit Work?

A is a vehicle that makes it simple to borrow money for a short time. Visa, Mastercard, Discover, and American Express are the primary card issuers all over the world.

What Does WECU Look at When I Apply?

When you apply for a credit card, the company issuing the card wants to make sure that you're able to pay back the money. So when you apply for your first card to provide this information:

1. Employment

2. Income

3. Debts—rent, car loans, student loans, etc

WECU then goes to one or more of the three credit reporting agencies—Equifax, Experian, or TransUnion—and gets a copy of your credit report. This report shows the following data:

4. Credit score

5. Credit history

6. Late payments

They make the decision on whether to issue you a Visa based on the info on the credit report, and your credit limit is determined by your credit score. The higher the score, the higher the limit. Most new Visa cardholders have a credit limit under $2,000. Major card issuers—Chase, Capital One, or Wells Fargo, for example—follow the same guidelines.

A Word About Credit Scores

Consumers grumble about the fairness of the credit scoring criteria in the US, and how hard it is to get your score. There are lots of apps you can download that tell you they can calculate your credit score, but those are mostly secondhand algorithms that have no basis in the real world of credit reporting. Creditors—the companies that lend you money—get a copy of your credit report whenever you apply for any kind of credit—landlords, cell phone companies, car dealerships—everybody.

Sometimes, they run a "soft" pull, which simply means it's for informational purposes and there's no specific loan application attached to the inquiry. A "hard" pull provides the same information, but the consumer has completed a credit application.

The credit application shows up on your credit report for two years. Even if it was approved and you decided not to buy the car or whatever, the inquiry shows up and it can negatively affect your overall score. Be very careful about applying for credit.

When Can I Ask For a Higher Credit Limit?

Every company has different guidelines about when you can apply for an increased credit limit. The general rule of thumb across the industry is no more than every six months. doesn't publish their rules for a bigger Visa limit but think about your overall financial health before you ask for an increase.

Additional Factors for WECU to Consider

Here's the thing. If your Visa account with WECU is in good standing, it will probably be fairly painless to get that increase.

- Do you pay the bills on time?

- Do you make more than the minimum payment?

They want to make sure that you can handle the additional payment amount. These are good indicators that you may qualify for a credit limit boost.

- New job, raise, or promotion

- Low credit usage

- Good credit score

Any financial institution likes it when you have a credit card and pay the balance every month—that's low usage.

When It's Best to Wait

The problem with credit limit increases is that when you need one, it may be hard to get. If you've lost your job or haven't made timely payments, you probably won't get the increase. Also, if they have approved a higher limit in the past six months, chances are good that you'll need to wait another few months for a boost.

Applying for a Credit Limit Increase at WECU

WECU makes the process simple. Fill out the application, and don't forget to include your current card number. You can also call the WECU service center and apply by phone. Here's the contact info for WECU.

| Phone Banking: | 360-756-7777 |

| Text: | 360-200-8442 |

| Email: | MemberServices@wecu.com |

| Street Address: | PO BOX 9750

Bellingham, WA 98227-9750 |

DoNotPay Makes it Easier

It's not like it's difficult to ask for a limit increase, it's just time-consuming and not all that easy to decide the best way to apply. Why not let DoNotPay apply on your behalf? Simply follow these steps and we'll take care of it for you—on your schedule.

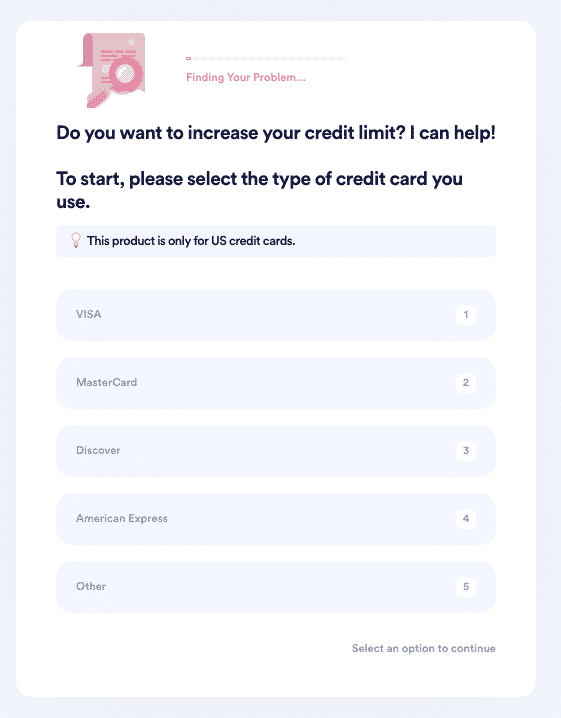

- Go to the Credit Limit Increase product on DoNotPay.

- Select which type of card you own and your credit provider.

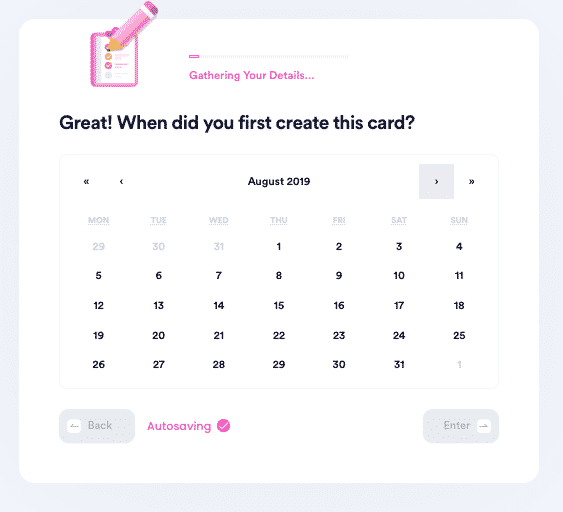

- Tell us more about your card, such as when you first created this card, your current credit limit, what you would like your new limit to be, your card number, and whether you've missed past payments.

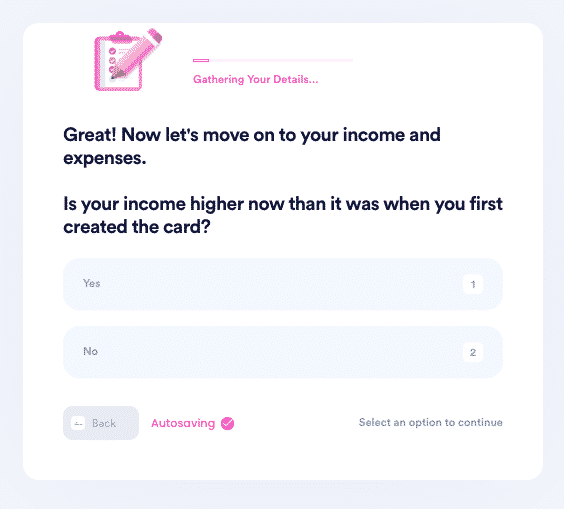

- Tell us more about your current income and expenses and why you would like to request a limit increase.

- Indicate whether you want to allow hard inquiries to be made into your credit history. Upload a copy of your ID and provide your e-signature

- Submit your task! DoNotPay will deliver the request letter on your behalf. You should hear back from the card provider with confirmation or a request for more information within a few weeks.

We can ask for increases for any other cards you may have, too. Just remember that hard inquiries can lower your score, so be careful about applications.

DoNotPay Is Like Your Personal Banker

In a world where banking is run by technology, DoNotPay is meeting the banks with our own super sophisticated AI. We can also help you with card refunds and chargebacks, better your understanding of the credit cards you need, and even file a complaint on your behalf. We do it all!

AI that fights for you

AI that fights for you