Request the Maximum Credit Limit for Your Citi Diamond Preferred Easily

If there's a Citi Diamond Preferred card in your wallet, you've already proven your creditworthiness. Citi requires a minimum 720 credit score to qualify for the Diamond Preferred card, and they also consider your overall debts and income before approving your application. Diamond cardholders have proven they can handle their finances, but what about when you need a higher credit limit? DoNotPay has the scoop on how you can have a and how you can increase your spending power.

Why Citi Diamond Is a Great Financial Tool

Unlike many credit cards, the Citi Diamond card does not have any rewards features. Instead, Citi has a different approach—it makes transferring balances very attractive. Here's how the card stacks up when you want to manage all your credit card debt with just one payment.

-

Prolonged Introductory APR Period

Citi Diamond sets itself apart from other cards in that its introductory period for transferred balances goes for 21 months at a zero APR (annual percentage rate). Wells Fargo's Reflect card offers the same rate and timeframe but demands an even higher credit score. Citi's Simplicity card also has an extended transfer period, but the interest rate is higher. True, it's only a point, but when you're carrying large balances, that adds up fast.

-

How Soon Must I Transfer Balances?

Citi requires that you transfer balances within 120 days to qualify for the introductory preferred rate. You get 12 months at zero interest for new purchases.

-

Competitive Interest Rate

Citi's Diamond Preferred card carries a variable interest rate between 13.74% and 23.74%. That's comparable to Citi's Simplicity card, but only if you're sure that you won't need Simplicity's waiver of a late payment fee.

-

The One Downside

The one drawback to the Diamond card is that the balance transfer fees are high—5%, with a $5 minimum.

You'll also be charged a balance transfer fee of 5% (minimum $5) based on the amount of each transfer, which could create a large upfront cost if you have to transfer a sizable balance. Let's do some quick math—if you transfer $12,000 in balances, then you'd pay $600 for moving the debt to Citi.

Weighing Your Options

Here are some things to consider if you're thinking of applying for a Citi Diamond Preferred card, or asking for the

-

Citi's Maximum Credit Limit

Citi does not publish the maximum amount of credit they offer on the Diamond Preferred card, but online chatter indicates over $15,000 is not uncommon. Considering that Citi is on the same playing field as American Express and the more elite Bank of America and Chase cards, highly qualified borrowers can probably name their own limit.

-

Making Your Decision

Here are some of the factors to consider if you're applying for a Citi Diamond card, or asking for an increased credit limit.

- Do you plan to pay the card off within 21 months?

- Are you planning a large purchase that you can pay off over a period of time?

- Will you need an increase in your credit limit to cover the transfer fees?

-

Are rewards important to you?

Lots of consumers prefer rewards cards, even if they're paying higher interest rates. Consumers typically use these cards for all their purchases and pay the balance every month, thereby earning thousands of points for travel with everyday expenses. If you travel a lot, Chase Sapphire is a great option, but if you just want cash back, American Express Blue Cash Preferred and Chase Freedom Unlimited are better options.

Asking Citi for a Higher Limit

You can ask Citi for an increase in your credit limit in one of these ways.

| By Telephone: | 1-800-950-5114 |

| By Email: | https://online.citi.com/US/ag/contactus |

| By Regular Mail: | Citibank Customer Service P.O. Box 6500 Sioux Falls, SD, 57117 |

| Online |

|

DoNotPay Figures It Out

Here's the thing—Citi is a stickler for that 720 plus credit score. If they pull your credit and it's under 720, then that inquiry goes on your report for two years, and it could make your score go down further. DoNotPay can make sure that Citi only pulls an informational report, which doesn't count against you.

We'll handle it for you with a click or two.

- Go to the Credit Limit Increase product on DoNotPay.

- Select which type of card you own and your credit provider.

- Tell us more about your card, such as when you first created this card, your current credit limit, what you would like your new limit to be, your card number, and whether you've missed past payments.

- Tell us more about your current income and expenses and why you would like to request a limit increase.

- Indicate whether you want to allow hard inquiries to be made into your credit history. Upload a copy of your ID and provide your e-signature

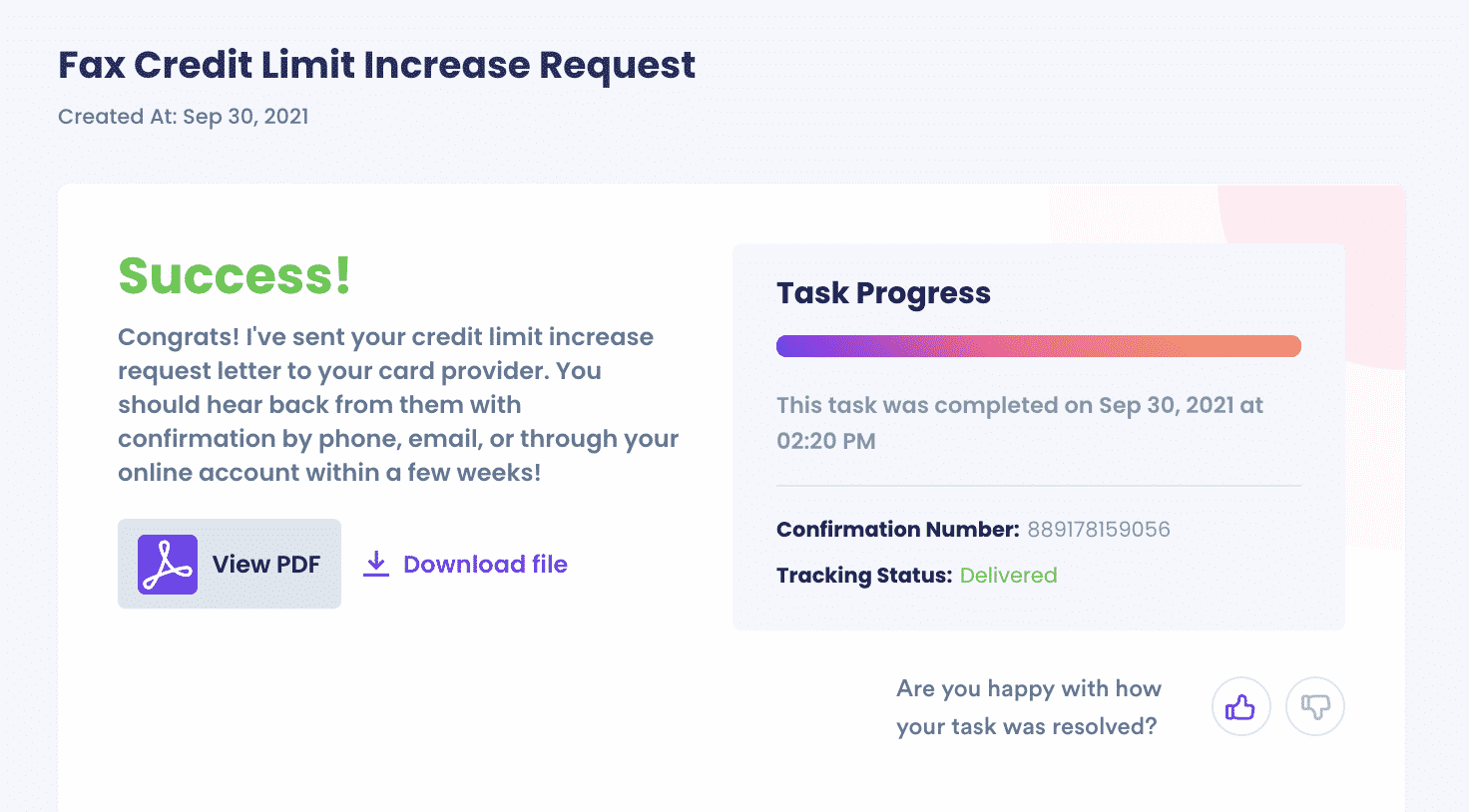

- Submit your task! DoNotPay will deliver the request letter on your behalf. You should hear back from the card provider with confirmation or a request for more information within a few weeks.

What Else Does DoNotPay Do?

Well, just about everything. We can help with retailer-branded cards, like

- Apple card

- Capital One

- Citi.Com

- Credit One

- and most other credit cards

If you have problems with purchases, we can get a chargeback or refund—something card companies hate to give. We're AI attorneys, so we're also pretty good at filing complaints, if necessary. DoNotPay simply makes it easier to deal with most business and government entities.

AI that fights for you

AI that fights for you